First Quarter 2016 Review

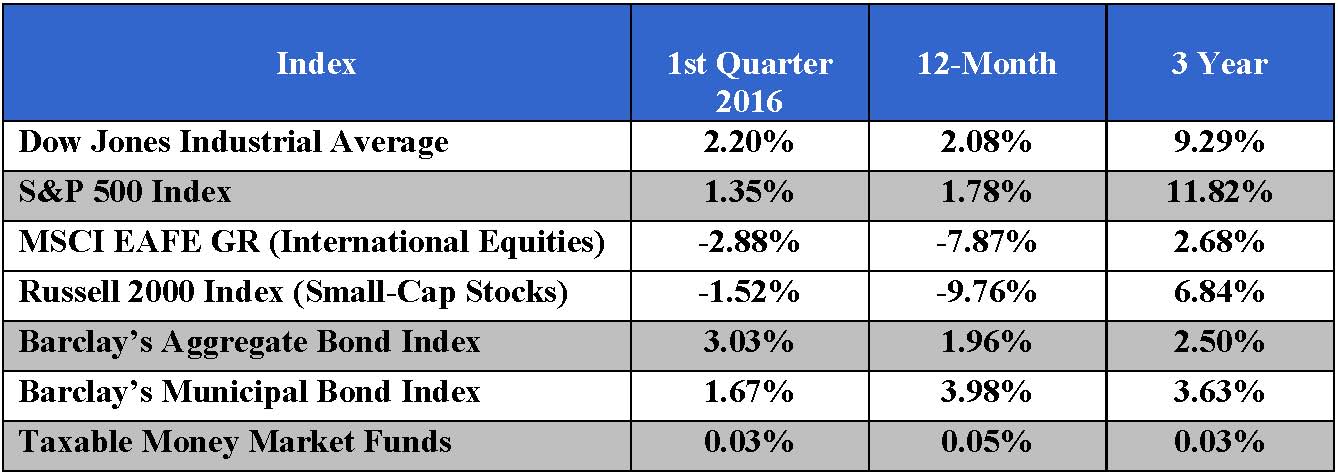

The market got off to a rocky start this year with equities down over 10% at one point, only to end the quarter up just over 1%. Concern over the pace of the Federal Reserve interest rate increases, declining oil prices, The United Kingdom’s potential exit from the European Union, and a slow down in emerging market economies, all contributed to the market volatility.

The Russell 2000 lost a little more than 1% for the quarter after being down close to 15% at one point. Smaller company and international stocks declined more than large company stocks, and international equities lost 3% for the quarter.

In the fixed income market, safe haven assets – such as U.S. Treasury bonds – fared well as investors sought the safety of Treasuries. The Barclays Aggregate Bond index, which is heavily weighted in Treasuries, gained about 3%. Municipal bonds continued to improve, returning about 1% for the first quarter, as investors sought tax-free income.

Money market rates are still close to 0%, while inflation in the U.S. was around 1% in the third quarter and close to 0% so far this year.

Since the first quarter of 2016 is also the year-to-date return, we have room in this report to show your annualized returns for the past three years. This is to remind everyone to focus on the longer term when it comes to portfolio performance. Time does cure extended periods of negative and flat portfolio performance. It also cures extended periods of higher than normal performance. For those of you who remember the late nineties, market returns were outrageously high and that was followed by a three year bear market of below normal returns, during the period 2000 to 2002. That bear market was followed by another multi-year bull market to bring the averages back to normal.

Major Market Indexes

Outlook and Strategy

Although oil prices seem to have stabilized for the time being, they are still very low, which is putting pressure on domestic oil and gas producers. There is concern about the flow through to the broader economy as individuals are laid-off in the energy and industrials sector. There is also concern about the corporate debt that won’t be paid as energy companies’ revenue declines.

While we continue to believe the U.S. Dollar will remain strong, there is a chance that, at least temporarily, the Dollar will decline slightly. This actually helps our multi-national companies’ earnings, and may do some good in bolstering near-term share prices.

We remain underweight international equities, which thus far has been the right strategy with the strong U.S. Dollar. In addition, many large U.S. domestic companies now have exposure to foreign currency volatility, so we see no need to raise our exposure at this time. Ultimately we have to pay our bills in U.S. Dollars, so taking on additional foreign currency risk does not make sense given the current risk/return environment. We are looking for opportunities to reduce direct foreign exposure and reinvest in low-cost domestic investment strategies. In addition, 45% of the S&P 500’s revenue is derived overseas which we feel is sufficient exposure without taking direct investments overseas.

Treasury yields remain near all-time lows but are still attractive when compared to negative interest rates in many developed economies overseas. This should provide a tailwind to intermediate-term fixed income indexes that are heavily weighted toward Treasuries. We expect municipal bonds to outperform as the prospects for higher income tax rates in the future seem likely, making tax-free income all the more attractive.

We remain cautious with our investment strategy. While there are more opportunities today than in the beginning of the year, the stock market remains fully valued. We continue to maintain a larger than normal cash position in our portfolios as we wait for opportunities to redeploy these assets. The current cash allocation is around 12% versus a normal level of 3% to 5%.

If you would like to speak with a Senior Wealth Advisor at R.W. Rogé & Company, Inc., please contact us at 631.218.0077. It would be our privilege to serve you and your family’s needs.