![]() By: Steven M. Roge, CMFC

By: Steven M. Roge, CMFC

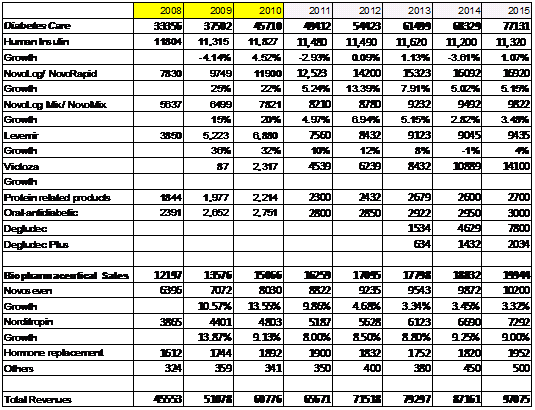

Business description and background

- Increasing risk of diabetes in parts of Asia

- Increasing treatment rates and early diagnosis in parts of BRIC nations, especially in China

- The proportion of patients treated by insulin is rapidly growing due to the ease of availability of insulin doses

- Start patients fresh with long-acting insulin on a new type of insulin and this could last longer with a longer patent protection. This could further translate into higher market share for Novo.

- Market leader, Sanofi-Aventis (SNY) long acting insulin (Lantus) is known to be a better performer than Levemir (Novo’s marketed long-acting insulin). This is further complicated by the fact that Levemir requires two doses a day. This perception would improve with the introduction of Degludec.

- •Lantus market share may decline from 53% to 30% by 2030 as a result of Degludec.

Additional disclosure: This discussion is for informational purposes and should not be taken as a recommendation to purchase any individual securities. Information within this discussion and investment determination of the author may change due to changes in investment strategy when warranted by changing market conditions, or if a security’s underlying fundamentals or valuation measures change. There is no guarantee that, should market conditions repeat, this security will perform in the same way in the future. There is no guarantee that the opinions expressed herein will be valid beyond the date of this presentation. There can be no assurance that the author will continue to hold this position in companies described herein, and may change any of his position at any time. We use or best efforts to obtain good data in our models, however it can’t be guaranteed that our inputs and data are correct. This is not a recommendation for readers to purchase shares in the above security without consulting your financial professional to discuss your own risk tolerance and objectives.